Finance 4.0 has been a recurring theme in almost every recent CFO forum and summit. But why have finance communities leaped to talk about Finance 4.0, when there were hardly any talks about Finance 3.0, 2.0, or 1.0 before?

One of the explanations is because of the trend and popularity of Industry 4.0. It seems like everyone is talking about the concept of a "4.0 world", such as Supply Chain 4.0, Marketing 4.0, HR 4.0, Education 4.0, Smart City 4.0, etc.

But what is the 4.0 world, exactly? And, how does it impact the finance industry?

In this article, I talk about the evolution of finance over 500 years and how the industry has evolved. I discuss key topics on the subject of financial evolution, including:

- What the 4.0 world is and why it's known as the fourth industrial revolution

- Finance in the 4.0 world

- Finance 4.0 in the context of the finance function

The 4.0 world

The 4.0 world is characterized by technological changes that are blurring the lines between physical, digital, and biological spheres. It is the cyber-physical systems that leverage the full integration of ICT (Information and Communications Technology) and Automation Technology.

In the 4.0 world...

- IoT (Internet of Things) is the source of big data. Cloud computing facilitates the storage and processing of large data sets. AI (Artificial Intelligence) enables advanced analytics.

- ML (Machine Learning) learns and identifies data patterns and makes predictive analytics to perform operations without human intervention.

- Blockchain enables cryptographic hash with transparent and independent distributed ledgers. This means that it can also secure transactions in the cyberworld.

- Cognitive computing mimics the functioning of the human brain to help to improve human decision-making.

Cognitive computing is the third era of computing. We went from the first era with computers that tabulate sums (the 1900s) to the second era with programmable computer systems (1950s).

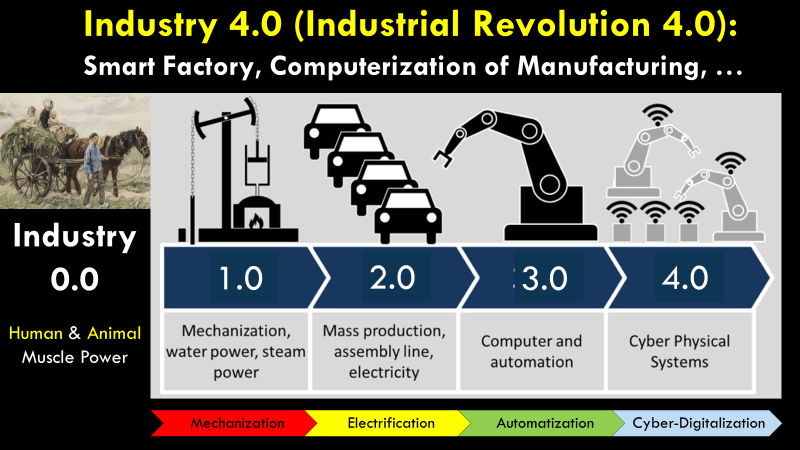

Industry 4.0 - The Fourth Industrial Revolution

In the olden days before Industry 1.0, we used the muscle power of humans and animals to run our operations. Then, the invention of the wheel increased the productivity of human and animal power.

Industry 1.0 started in the late 18th century when steam power and water power revolutionized our industry. This is the era called Mechanization.

Industry 2.0 occurred in the 19th century when electricity and assembly lines brought the concept of mass production with specialization of skills. This is the era called Electrification.

Industry 3.0 started with robust industrial processes and quality control systems. Both were supported by the advances in computing that allowed us to program machines and networks. This is the era called Automation.

Industry 4.0 is the Cyber-Physical system that leverages the full integration of ICT (Information and Communication Technology) and Automation Technology. This is called the Cyber-Digitalization era with the convergence of Information Technology with Operational Technology.

There is a clear universal standard definition of the industrial revolution from 1.0 to 4.0. Therefore, we will not elaborate in detail as the information is easily available. On the contrary, there is no universal standard to describe Finance 4.0.

Finance 4.0 - Finance in the 4.0 World

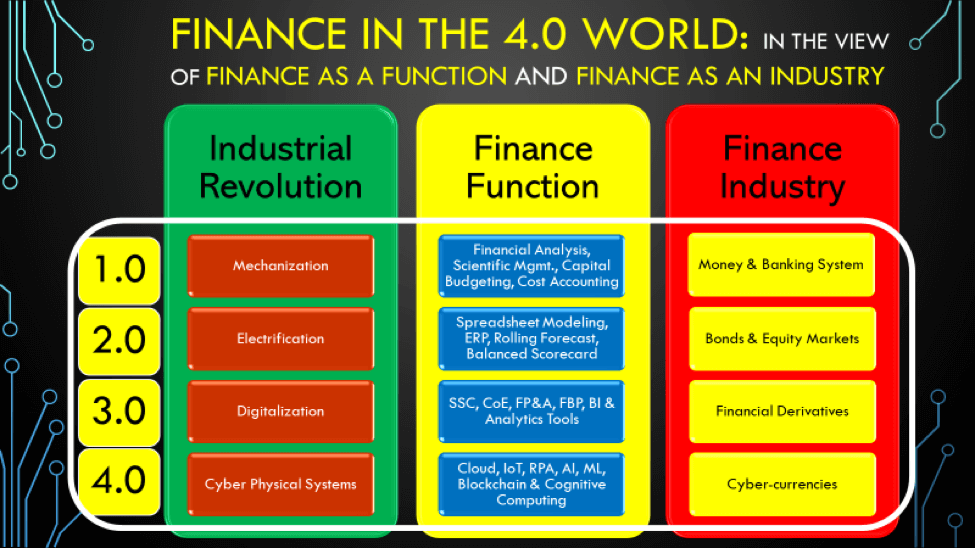

Just like the industrial revolution, finance is also going through several stages of revolution. Due to the wide scope definition of finance, there is no universal standard description of finance evolution. It is better to describe it as finance evolution not finance revolution.

In this article, I will describe the finance evolution into two main categories: finance as an industry and finance as a function. Here is a simplified chart to summarize these key evolutions:

Finance 4.0 in the context of the Finance Industry

Finance 1.0: Finance is a derivative of the economy with its purpose to facilitate business operation. Hence, it is not by chance that the central banks were established at the start of the First Industrial Revolution. This era is called Finance 1.0 in the finance world.

Finance 2.0: It started with the emergence of credit & equity markets. Industrialization and colonization came at the same time as the globalization of banks, stocks, and bond markets.

Finance 3.0: With the invention of telecommunication equipment, the telex and fax machines, followed by the internet (which speeded up information transmission in the 1980s), the finance industry entered into the information technology age.

The advent of the internet and financial derivatives gave birth to Finance 3.0. These financial derivatives were quite vulnerable. They can be manipulated for tax and regulation evasions. The creation of financial derivatives with a very complex structure and highly leveraged referred to as “the weapons of mass destruction” by Warren Buffet.

The main reason why he named it as such is that it brought the world’s financial markets down. The global financial crisis in 2007 had to be rescued with help from the central bank's intervention. This was accomplished using unconventional monetary policy and with unprecedented interest rates.

Finance 4.0: Fast forward, we are now entering Finance 4.0, which is about utilizing digital technology to drastically change the global financial market. This fastest and most dramatic change in the financial products (digital wallets, mobile payment, etc.) and the financial systems sparked by the new digital technologies are challenging the existence of century-old legacy financial institutions and redefining the framework of trust in the banking system. It redefined the world where economic and consumer power is globally distributed.

The arrival of blockchain or distributed ledger technology with the invention of cyber-currencies or crypto-currencies (bitcoin, Ethereum, etc.) makes cross-border transactions easier.

Decentralized finance (“DeFi”) has been a positive catalyst for the increased adoption of Ethereum’s network. By leveraging ether as “trust-minimized” collateral, market participants can disintermediate traditional financial companies and access financial services like credit & lending, market making, trading, custody, investing, and access to synthetic US dollar exposure.

DeFi with the key components: blockchain, cryptocurrency, smart contracts, stablecoins, and decentralized applications (dApps) will democratize finance to solve: inefficiency (costly, slow, and insecure transactions,) limited access (1.5 billion of the population are unbanked or underbanked,) opacity (the needs to trust regulators to monitor banks,) centralized control (oligopolistic financial system imposing higher fees than the real competitive market fee) and lack of interoperability (difficulty in funds movements among financial institutions.)

Finance 4.0 will certainly increase the volume and velocity of financial transactions. However, will this development lead us to another massive financial crisis or help us to avoid it?

When the next financial crisis strikes in the future, the magnitude might be a lot worse than the previous one. It had been speculated that the next financial crisis might be caused by the collapse of the digital ecosystem in the finance industry either due to incorrect applications or cybercrime attacks. In the 4.0 world, a cyber security risk is not just a tech risk, it is also a business risk.

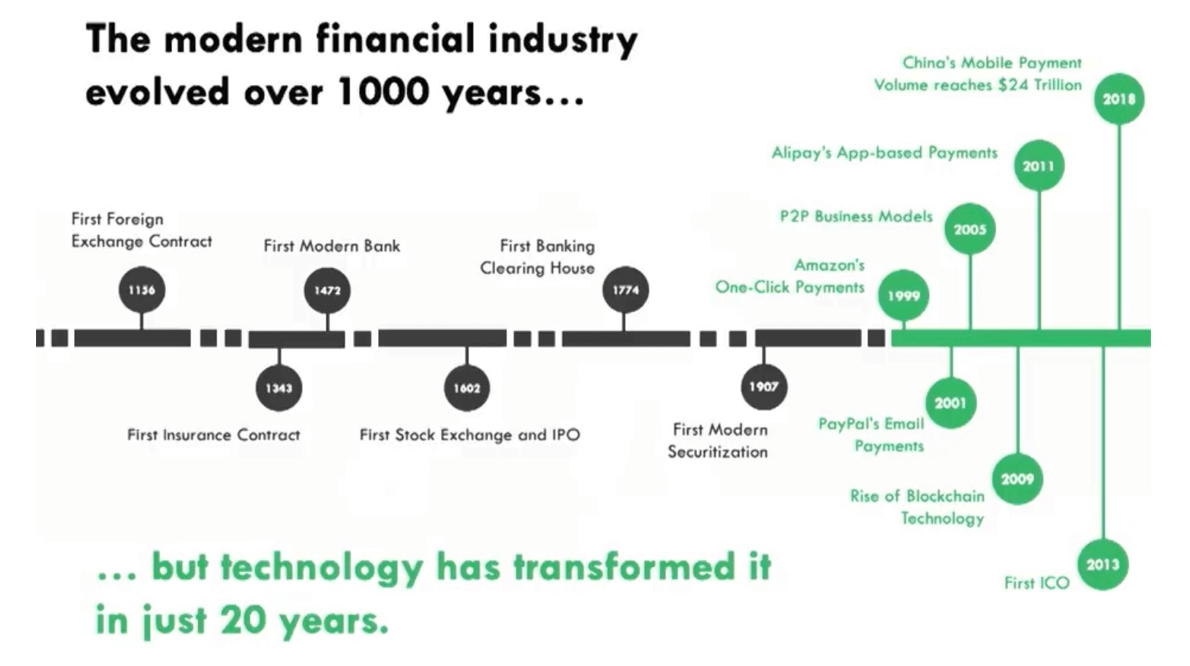

Below is a summary of the finance industry evolution over 1000 years by ARK-Invest.com.

It is amazing to see how technology has transformed the finance industry in the last 20 years. This Finance 4.0 era is also referred to as the FinTech era in the finance industry.

Finance 4.0 in the context of Finance Function

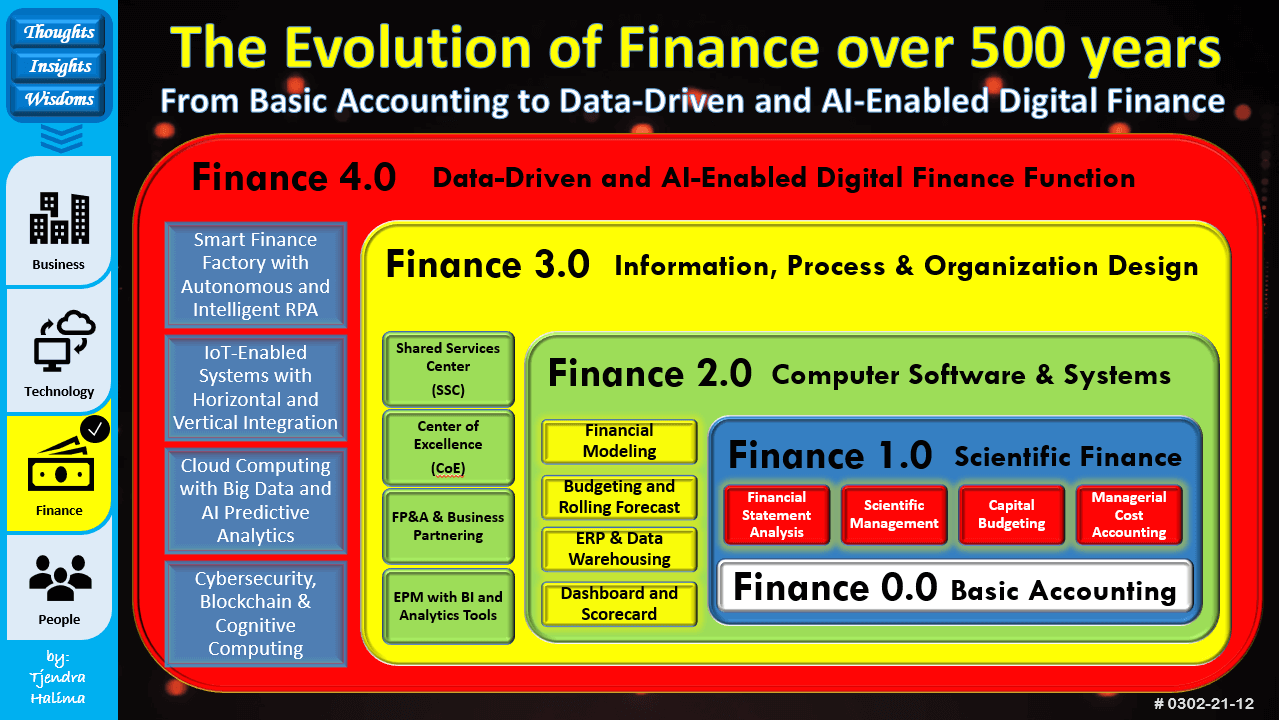

Financial Accounting started more than five centuries ago (1494) when Luca Pacioli, the father of accounting, introduced double-entry accounting. This is the era long before the 1.0 world. We can call this the Finance 0.0 era.

During the Industrial Revolution in 1700-1900, accounting took off as industrial companies sought to gain financing and maintain efficiency through operations. Several of the double-entry accounting methods were truly developed in this area as there was a focus on business as never before.

Finance 1.0: the Scientific (Mathematical) Finance era

The arrival of PCs played a vital role in the evolution of finance. It carried out a financial statement analysis using various ratios to understand the financial health of an organization.

The scientific management techniques leveraging mathematics (statistics, calculus, linear programming, etc.) were also adopted. Capital budgeting with the time value of money (PV, FV, DCF, IRR) concepts was also introduced in financial decision-making to maximize the returns.

Management and cost accounting were introduced to support industrial operation (from the assembly line to mass production) and different manufacturing methods (from discrete to process manufacturing) with costing information, variance analysis, breakeven analysis, sensitivity analysis, over-under absorption, etc.

Finance 2.0: the Computer Software and Systems era

With the increases in computer processing power & speed, a sophisticated spreadsheet was invented that enabled financial modeling. The use of sophisticated functions in spreadsheets nurtured the Rolling Forecast concept, what-if analysis, scenario planning, balanced scorecard, etc.

On the system side, ERP (Enterprise Resource Planning) and data warehousing were introduced after the Y2K crisis to solve the island of computerization issues where every department worked in SILO and maintained independent systems with their own set of data and information.

Finance 3.0: the Information, Process, and Organization Design era

With the maturity of ERP implementation, the finance function started to look for cost savings and process efficiency by introducing SSC (Shared Service Center), BPO (Business Process Outsourcing), and GBS (Global Business Services) to streamline and standardize processes: P2P (Purchase to Pay), O2C (Orders to Cash), R2R (Record to Report), etc. CoE (Centre of Excellence) organization was also introduced to mutualize and share the expert functions.

With basic accounting tasks being done by SSC and tasks that required expertise being done by CoE, the finance function could reallocate its resources from back-end to front-end and started to look for opportunities to be visible in the business and operation by introducing FP&A (Financial Planning & Analysis) and FBP (Finance Business Partnering) functions.

On the system side, we started to see the booming of ERP add-ons and BI (Business Intelligence) tools with advanced analytics for better business insights and foresight.

The finance function had come a long way in pursuing technology transformation, from islands of computerization to integrated ERP systems. Today, we are enriching the core ERP systems with BI tools. These BI tools with analytics capability and with the availability of big data have enabled us to look beyond traditional finance. These have resulted in the introduction of EPM (Enterprise Performance Management) systems.

Finance 4.0: the Data-Driven and AI-Enabled Digital Finance era

With the advance in digital and automation technologies, robotic process automation (RPA,) artificial intelligence (AI,) machine learning (ML,) cloud, and analytics, the finance function is now able to deliver significantly more value to the business – quickly, in real-time, at greatly reduced cost with higher levels of automated control and lower risk.

Finance leaders are now leveraging on RPA to industrialize finance just like factories with digital assembly lines & mass production. RPA is already taking over high volume repetitive and monotonous work in the shared service center (SSC). Hence, the role, size, and shape of SSC will change.

It will be smaller, more efficient, and cost less but with a higher proportion of highly skilled people to run the SSC. RPA is also enabling the center of excellence (COE) to step up and focus on advanced analytics to provide in-depth business insights enabling better decision-making.

RPA powered with AI will enable organizations to synthesize a vast amount of structured and unstructured financial and non-financial data, query results in natural language, and apply machine-learning capabilities to data analysis. Together, these capabilities can significantly enhance insights, efficiency, and speed. Reporting the past will become more efficient, allowing finance to shift their mindset to the future and create value for the business.

Today, there is still a disconnection between the old-world ERP and the new-world IoT. It is estimated that even the most advanced ERP system is only consuming around 15-20% of IoT data, limiting the huge digital transformation potential of IoT.

The ERP systems have been on the information technology (IT) scene for many years and were not designed to handle big unstructured data from networks of distributed devices and sensors in the fields and shop floors. However, the exponential rise of the Internet of Things (IoT) in every corner of business operation is opening a new frontier for enterprises to have IOT-enabled and Integrated Enterprise Management Systems or an EDP (Enterprise Digital Platform.)

The backbone of EDP is horizontal and vertical integration. With horizontal integration, processes are tightly integrated at the field level across the entire organization. With vertical integration, all layers in the organization are tightly connected.

This EDP will mine big data for predictive analytics with AI & ML and will provide the ability to extend big data collected from the distributed assets or devices in the fields to the C-Suite for operational and strategic decision making. Hence, data can flow freely from the shop floor to the top floor and vice versa.

Last but not least, Finance is now starting to look at how to utilize and apply Blockchain and Cognitive Computing in the finance and business world. Cognitive computing is the next-generation information system that understands, reasons, learns, and interacts. It continually builds knowledge and learning, understanding of natural language, and reasoning and interaction more naturally with human beings than traditional programmable systems.

"Finance transformation to 4.0 world is driven by People, facilitated by Processes, enabled by Technology, and fueled by Data. People are the most important contributor to the success in the transformation journey to the Finance 4.0 world." - Tjendra Halima

Marisa Garanhel

Marisa Garanhel

AI accelerator insider insider

Thank you for subscribing

Level up your ai accelerator insider career & network with ai accelerator insider experts.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn